CapEx Is Not an Expense

- Hurratul Maleka Taj

- May 15

- 6 min read

Updated: May 17

What Big Tech's $700 Billion Infrastructure Bet Tells Us About How Markets Think

On April 29, 2026, the four largest technology companies in the world, Microsoft, Alphabet, Meta, and Amazon reported earnings on the same day. All four raised their capital expenditure guidance. The combined bill for 2026 is now tracking between $650 and $700 billion, the largest concentrated infrastructure cycle in the history of private enterprise.

The markets did not react uniformly. And that divergence is the most important story.

The Accounting Concept We Need to Understand

Before reading market reactions, one distinction must be made precise: capex is not an expense in the income statement sense. It is an asset acquisition. It sits on the balance sheet, gets depreciated over its useful life, and generates future productive capacity.

At the point of spending, capex never hits the income statement as an expense. When a company allocates capital to infrastructure, it is recorded as an asset on the balance sheet, depreciated over its useful life, with only that depreciation appearing on the P&L gradually over years. On the cash flow statement it sits under investing activities, not operating activities, which means it is categorically separate from the day to day cost of running the business.

Conflating capex with operating expenditure is not just imprecise. It is analytically consequential, because it leads you to the wrong conclusion about what the market is actually doing when it reacts to these announcements.

The market is not running a revenue-minus-expense calculation. It is pricing something far more specific: the credibility of the return timeline on each company's capital deployment.

The Evidence: Four Companies, Three Different Verdicts

Alphabet jumped nearly 10% on April 30, the day after its earnings release. This despite raising its 2026 capex guidance to $180 to $190 billion and signaling that 2027 capex would increase further still. The reason the market rewarded it rather than punished it: Google Cloud crossed $20 billion in quarterly revenue for the first time, growing 63% year over year, with a contracted backlog of $460 billion, nearly double the prior quarter. The capex had a visible, contracted demand anchor. The return timeline was legible.

Microsoft beat analyst expectations on both revenue and earnings per share, yet its stock fell roughly 4 to 5% on April 30. The market's attention went instead to its $190 billion capex forecast for 2026, a 61% increase from the prior year and 23% above what analysts had been expecting. Microsoft's AI revenue run rate of $37 billion annualized, growing 123% year over year, provided partial reassurance, but the scale of the spend created uncertainty about the free cash flow bridge.

Meta reported revenue up 33% year over year, beating consensus. The stock fell approximately 8 to 9% in the following trading session, entirely because capex guidance was raised to $125 to $145 billion for 2026. Meta's revenues were strong. The market still sold it. Under a revenue-minus-expense framework, this reaction makes no sense. Under a capital allocation confidence framework, it makes complete sense: Meta's capex is building consumer AI infrastructure whose payback runs through internal advertising systems, not a third-party cloud with contracted revenue. The yield horizon is less transparent to institutional investors.

The Production Possibilities Frontier: What Economics Actually Tells Us

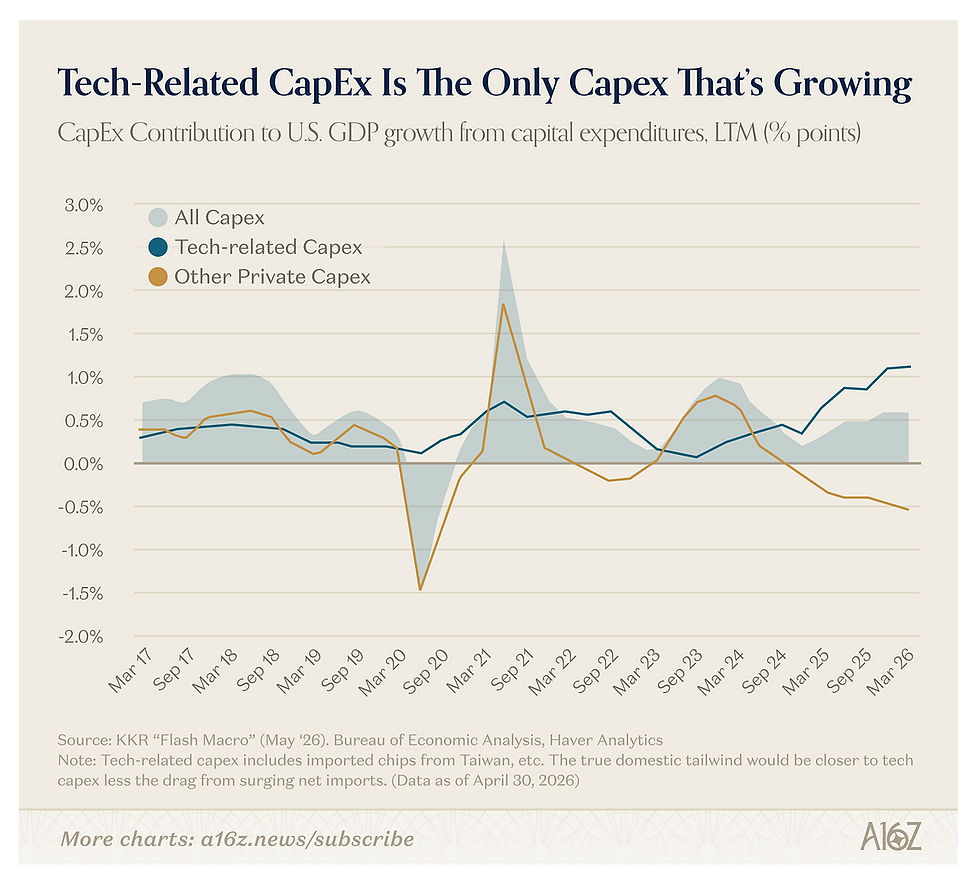

Source a16z: “KKR estimates that tech-related capex is the only kind of capex currently contributing to growth (and it’s contribution is growing)—in fact, tech capex contributed 1.9% of the 2% total GDP growth in Q1, i.e. basically all of it.

But, tech investing is bigger than just capex, and its role in the economy is bigger than its recent contributions to GDP.

By the BEA’s measure of total business capital expenses (which includes R&D and software, in addition to capex), tech is now 55% of all business investment in the US”

This is not just a market pricing story. It is a macroeconomic one. The chart from a16z and KKR's Flash Macro (May 2026) makes the structural point with precision: tech-related capex is the only category of capital expenditure currently contributing positively to US GDP growth, accounting for nearly all of the 2% growth recorded in Q1. All other private capex is flat or contracting.

In economic terms, what these companies are doing is not consumption. It is capital formation, the mechanism by which the production possibilities frontier shifts outward. An economy, or a company, that consumes its resources stays on the same frontier. One that invests in productive infrastructure expands what is achievable. The distinction between consumption expenditure and capital formation is foundational in national income accounting, and it is precisely what the market is attempting to price, imperfectly, in real time.

What the Divergence Tells Us

The market is not anti-investment. It is not punishing companies for spending. It is asking one question with increasing precision: when does this frontier expansion yield a return, and how visible is the compounding mechanism?

Alphabet answered that question clearly on April 29. Microsoft partially answered it. Meta has not yet answered it in a way institutional investors can model quarter by quarter.

The market is now pricing each hyperscaler on the strength of its AI revenue evidence, not on the scale of its capex commitment alone.

That is a precise distinction. It is also the correct one.

The companies that survive and win this infrastructure cycle will not be the ones that spent the most. They will be the ones whose capex built a moat that is irreplaceable by the time the frontier shifts again. The stock market, for all its short-termism, is trying to figure out which is which.

CapEx, Free Cash Flow, and Why Markets React So Differently

This distinction becomes even more important once free cash flow enters the picture.

Capex may not be an operating expense in accounting terms, but it is still a real cash outflow. Every additional dollar spent on AI infrastructure immediately affects free cash flow, financing flexibility, and the timing of shareholder returns. That is why markets can react negatively to strong earnings when capital expenditure guidance rises aggressively.

In practical terms, investors are constantly asking three questions simultaneously:

How much cash is leaving the business today?

How long will it take for that infrastructure to generate incremental cash flows?

How visible and underwritable is the return on that invested capital?

This is where the divergence between Alphabet, Microsoft, and Meta becomes analytically important.

Alphabet’s capex was interpreted as relatively lower-risk because the monetization pathway was already visible through contracted cloud demand, enterprise AI adoption, and backlog expansion. Investors could see the near-term free cash flow compression, but they could also model the likely return stream with greater confidence.

Microsoft sat somewhere in the middle. The company demonstrated strong AI revenue growth, but the magnitude of its infrastructure build-out created uncertainty around the duration of the free cash flow compression cycle and the eventual return profile.

Meta presented the hardest case for institutional investors to underwrite. The company’s revenues were strong, but much of the AI infrastructure investment is being directed toward long-duration consumer and advertising ecosystems whose monetization pathways are inherently more difficult to forecast quarter by quarter.

This is why two companies can raise capex guidance and receive completely different market reactions.

The market is not simply rewarding or punishing spending itself. It is evaluating whether current cash outflows are likely to compound into durable future cash flows at attractive returns on invested capital.

That is fundamentally a capital allocation judgment, not a simplistic expense calculation.

This is also where net present value becomes the operative framework. A company's intrinsic value is the sum of its future free cash flows discounted back to today. When capex guidance rises aggressively, it compresses near-term free cash flows, which mechanically reduces the NPV calculation unless the market believes the future cash flows generated by that investment will more than compensate. Alphabet's stock held because the market revised its future cash flow estimates upward. Meta's fell because the market was not yet willing to make that revision with confidence. The stock price reaction was not an expense judgment. It was an NPV judgment.

Sources: Alphabet Q1 2026 Earnings Release, CNBC (April 29, 2026); Microsoft Q3 FY2026 Earnings, CNBC (April 29, 2026); Meta Q1 2026 Earnings, CNBC (April 29, 2026); KKR Flash Macro, May 2026, cited in a16z; Big Tech Q1 2026 Earnings Overview, Gotrade News (April 29, 2026).

References:

Alphabet Q1 2026 Earnings Release (Official IR) https://abc.xyz/investor/news/news-details/2026/Alphabet-Announces-First-Quarter-2026-Results-2026-X-ge4Dm6bf/default.aspx

Alphabet Q1 2026 Earnings, CNBC (April 29, 2026) https://www.cnbc.com/2026/04/29/alphabet-googl-q1-2026-earnings.html

Alphabet Q1 2026 SEC Filing (Form 8-K Exhibit 99.1) https://www.sec.gov/Archives/edgar/data/0001652044/000165204426000043/googexhibit991q12026.htm

Microsoft Q3 FY2026 Earnings, CNBC (April 29, 2026) https://www.cnbc.com/2026/04/29/microsoft-msft-q3-earnings-report-2026.html

Microsoft Capex Analysis, Motley Fool / Yahoo Finance https://finance.yahoo.com/markets/stocks/articles/microsofts-capex-spending-2026-23-135000219.html

Meta Q1 2026 Earnings, CNBC (April 29, 2026) https://www.cnbc.com/2026/04/29/meta-q1-earnings-report-2026.html

Big Tech Q1 2026 Earnings, $700B AI Capex Overview, Gotrade News (April 29, 2026) https://www.heygotrade.com/en/news/big-tech-q1-2026-earnings-ai-capex-spree/

KKR Flash Macro, May 2026, "Tech-Related CapEx Is The Only Capex That's Growing," cited in a16z newsletter https://www.a16z.news/p/charts-of-the-week-it-was-a-good

Comments